🎲 Martingale: When Mathematics Tries to Beat Randomness

Have you ever heard the strategy of “doubling your bet after every loss”? That’s precisely the martingale — a concept that originated in 18th-century French casinos and became foundational to modern probability theory.

📐 What is a martingale? In probability theory, a martingale is a stochastic process where the expected value of the next observation, given all past observations, equals the most recent value. Simply put: the best forecast for tomorrow is today’s value, regardless of history.

💡 Real-world examples:

- A symmetric random walk: at each step there’s an equal probability of going left or right

- A gambler’s fortune in a fair game: no matter the past wins or losses, the expected future value always equals the current fortune

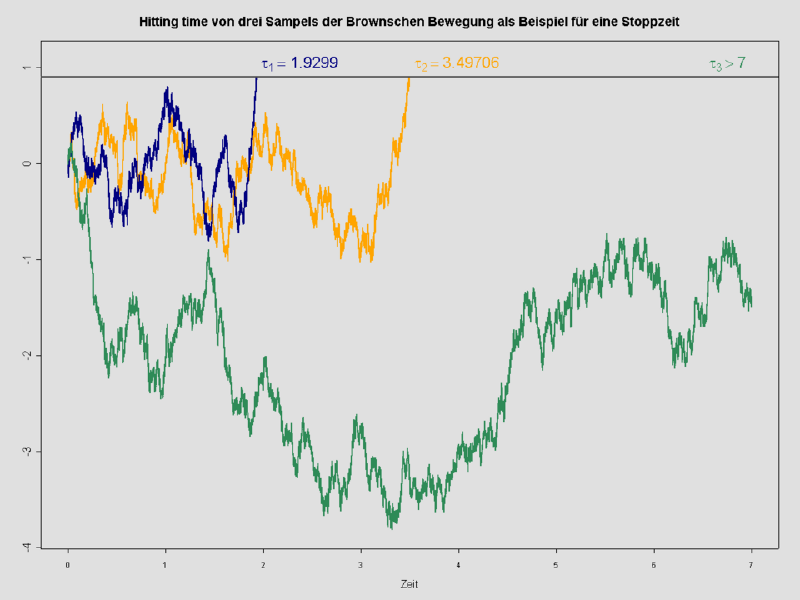

- Stopped Brownian motion: models physical and financial trajectories

🔍 Explanation in a nutshell Imagine flipping a fair coin and betting $1 each time. The classic martingale strategy says to double your bet after every loss ($2, $4, $8…). With infinite capital and infinite time, you’d always win eventually — but in the real world, bets grow exponentially and you run out of money first. The mathematics proves that no strategy can turn an unfair game into a long-term winner.

📈 Today, martingales are essential in quantitative finance, in options pricing theory (the Black-Scholes model), and in the analysis of machine learning algorithms.

More information at the link 👇